Assessed Value vs. Market Value in Texas: What's the Difference — and Why Does It Matter?

The number on your county tax record and the number your home would actually sell for today are two completely different things. Mixing them up can cost you — whether you’re a seller who underprices their home, a buyer who thinks they’re getting a deal, or a homeowner overpaying on taxes you could protest.

Let’s break it all the way down.

|

THE SHORT ANSWER: Assessed value is set by the county for your tax bill. Market value is what a buyer will actually pay for your home today. They are almost never the same number — and in Texas, the assessed value is typically LOWER than market value thanks to homestead exemptions and caps. |

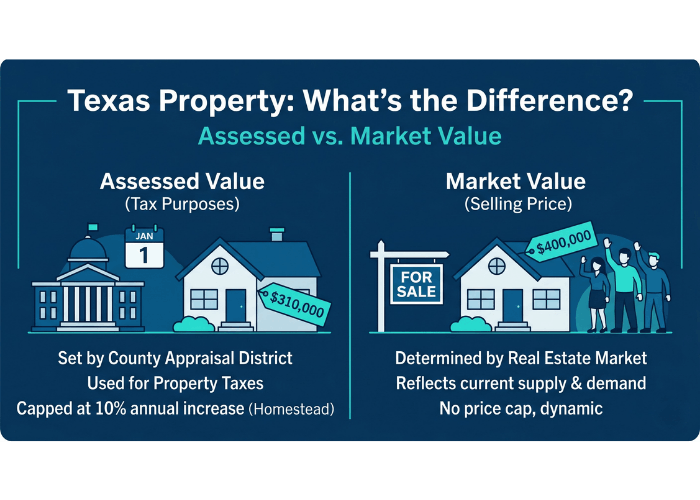

What Is Assessed Value? (And Why Your Tax Bill Uses It)

Assessed value — also called tax-appraised value — is the value your county appraisal district assigns to your property for the purpose of calculating your annual property tax bill. In Texas, this is handled by your county’s County Appraisal District (CAD). For example:

- Harris County homeowners include but is not limited to, Houston, parts of Friendswood, parts of Clear Lake and more.

- Brazoria County Appaisal District (BCAD) homeowners include but is not limited to Pearland, Manvel, Rosharon and beyond.

- Galveston County Appraisal District (GCAD) homeowners include but is not limited to Friendswood, League City, Texas City, La Marque, Dickinson and beyond.

Each January 1st, the appraisal district takes a mass snapshot of your property’s estimated value. This becomes your “appraised value” for that year. Your “assessed value” is then that number minus any exemptions you qualify for — like the homestead exemption, the over-65 exemption, or the disabled veteran exemption.

The assessed value is then multiplied by your local tax rate to produce your annual property tax bill. That’s its entire job.

The Texas 10% Homestead Cap — A Big Deal

One of the most important things to understand about Texas property taxes is the homestead cap. If your home is your primary residence and you have a homestead exemption on file, the county appraisal district cannot raise your assessed value by more than 10% per year — no matter how fast the market is moving.

This means that in years where the market surged (like 2020–2022 when Southeast Houston values jumped 25–35%), many homeowners’ assessed values lagged well behind their actual market value. A home worth $400,000 on the market might have an assessed value of only $310,000 if the cap had held the increases back over several years.

This is great news for your tax bill. But it also means the number you see on your county records is NOT a reliable indicator of what your home would sell for.

|

2026 UPDATE — TEXAS HOMESTEAD EXEMPTION INCREASE: |

What Is Market Value? (And Why It’s What Actually Matters)

Market value is the price a ready, willing, and able buyer will pay for your home in today’s market — and what a ready, willing, and able seller will accept. It reflects real-world supply and demand, current interest rates, the condition of your specific home, and what comparable homes nearby have actually sold for.

Market value isn’t set by a government office. It’s set by the market itself — through actual transactions between buyers and sellers. A skilled real estate agent determines market value through a Comparative Market Analysis (CMA), which looks at:

• Recent sales of comparable homes in the same area (comps)

• Active listings competing with your home right now

• The condition, age, and features of your specific property

• Current days on market and absorption rates in your neighborhood

• Buyer demand trends in your price range

Market value is the number that matters when you’re buying or selling. It’s what your lender’s appraiser will assess during the mortgage process. It’s what buyers are willing to write a check for. And it’s what determines whether you walk away from closing with equity — or not

Side-by-Side: Assessed Value vs. Market Value

Here’s a clear comparison of how these two values differ:

|

|

Assessed / Tax Value |

Market Value |

|

Set by |

County Appraisal District (CAD) |

The real estate market – buyers & sellers |

|

Used for |

Calculating your property tax bill ONLY |

Pricing, offers, negotiations, lender appraisals |

|

Updated |

January 1st each year by the CAD |

Constantly, based on sales activity |

|

In Texas |

Capped at 10% annual increase (homestead) |

No cap, reflects actual price |

|

Typical relationship |

Usually LOWER than the market value |

Usually HIGHER than assessed value |

|

What is tells you |

What your country thinks it’s work for tax purposes |

What a buyer will actually pay today |

A Real Example — Pearland, Texas

Let’s make this concrete. Say a homeowner in Pearland bought their home in 2016 for $255,000. They filed for a homestead exemption, so BCAD has been capping their assessed value increases at 10% per year. Fast-forward to 2025:

|

HYPOTHETICAL EXAMPLE: County Tax Record (BCAD): $295,000 assessed value Actual Market Value based on comparable sales: $375,000 Difference: $80,000 — or roughly 27% below what buyers will actually pay. If a buyer looked at that tax record and thought they were getting a $295,000 home, they’d be in for a surprise when they made an offer and found out comparable homes are selling for $370,000–$380,000. Equally, if that seller priced their home at or near the assessed value, they’d be leaving tens of thousands of dollars on the table. |

This is why I always run a full Comparative Market Analysis for every buyer and seller I work with — never relying on tax records to determine what a home is worth in today’s market.

What This Means for Sellers

If you’re thinking about selling your home in Pearland, Friendswood, League City, or anywhere in Southeast Houston, here’s what you need to know:

• Your county tax record is NOT your list price. Pricing your home based on assessed value almost always means leaving money on the table.

• Market value is set by what buyers are actually paying for comparable homes right now — not by what the county thinks it’s worth for tax purposes.

• A professional CMA from a local REALTOR® is the most accurate way to understand what your home will sell for in today’s market.

• In a balanced or buyer-friendly market like 2025–2026, accurate pricing is even more critical. Overpriced homes sit. Correctly priced homes sell.

I’ve seen sellers in our market leave $30,000–$80,000 on the table by underpricing based on tax records — and I’ve also seen sellers overprice based on the 2022 peak and watch their home sit for 90+ days. Neither outcome is good. The goal is accurate pricing grounded in current market data.

What This Means for Buyers

If you’re buying a home in Southeast Houston, here’s the key thing to understand:

• A low assessed value does NOT mean the home is priced at a deal. You will pay market value — what comparable homes have sold for — not what the county says it’s worth for taxes.

• Always ask your agent to pull comps before making an offer. This is the only reliable way to know if a home is fairly priced.

• When your lender orders an appraisal, it will be based on comparable sales (market value), not the county tax record. If the appraisal comes in below the contract price, it can affect your financing.

• Understanding this difference gives you negotiating power. If comps support a lower price than the list price, your agent can use that data to negotiate on your behalf.

|

BUYER TIP: One of the first questions to ask when touring a home is: “What have comparable homes sold for in this neighborhood in the last 90 days?” That’s your real benchmark — not the county tax record. |

What This Means for Homeowners — You Can Protest Your Assessed Value

Here’s a piece of information that could actually save you money: if your county’s assessed value is too HIGH relative to what your home would sell for, you have the right to protest it every year.

In Texas, the protest deadline is typically May 15th (or 30 days after your Notice of Appraised Value is mailed, whichever is later). You can protest online, by mail, or in person at your county appraisal district.

Successful protests use comparable sales as evidence — the same comps your real estate agent would use to price your home. If similar homes in your neighborhood sold for less than your assessed value, that’s grounds for a reduction.

Why does this matter? Every dollar your assessed value is reduced translates directly to lower property taxes. In a year when markets are softening, your county’s assessed value might not reflect current market conditions. Protesting is how you correct that.

|

2027 PROTEST REMINDER: The protest window in most Texas counties closes May 15, 2027 (or 30 days after your notice arrives). If you received a Notice of Appraised Value that seems too high, consider filing a protest. A real estate professional who knows your neighborhood can help you gather the comparable sales evidence you need. |

The Third Number: Lender Appraised Value

You may also hear the term “appraised value” used in a completely different context during a home purchase: the lender’s appraisal. This is a third and separate concept worth understanding.

When you’re buying a home with a mortgage, your lender orders an independent appraisal from a licensed appraiser. This appraisal estimates what the home is worth based on — you guessed it — comparable sales. Its job is to protect the lender by confirming the home is worth at least as much as the loan amount.

This lender appraisal is different from your county’s appraised value. It’s based on current market conditions and recent sales, just like a CMA. If the lender’s appraisal comes in below the contract price, the buyer and seller may need to renegotiate.

In short, there are three separate “values” your home might have at any point in time:

• County assessed / tax value — for your property tax bill

• Market value — what buyers will pay, determined by comps

• Lender appraisal value — the lender’s independent estimate to protect their loan

Understanding which number applies in which situation is exactly the kind of thing your REALTOR® is here to help you navigate.

The Bottom Line

If you take nothing else from this post, remember this:

• The number on your county tax record is NOT what your home is worth on the market.

• Market value is what buyers actually pay, and it’s almost always higher than assessed value in Southeast Houston.

• Sellers who price off tax records leave money on the table. Buyers who trust tax records can make costly mistakes.

• You can protest your assessed value each year if it doesn’t reflect current market conditions.

• A local REALTOR®’s Comparative Market Analysis is the most accurate tool for understanding what your home is worth today.

Whether you’re thinking about selling, buying, or just want to know what your home is really worth in today’s market — I’m always happy to run a no-obligation CMA and walk you through the numbers.

|

READY TO KNOW YOUR HOME’S REAL MARKET VALUE? I offer free, no-obligation Comparative Market Analyses for homeowners throughout Pearland, Friendswood, League City, Webster, Manvel, and the greater Southeast Houston area. Call or text me at 832-890-3504, email shelley@shelleybtxrealtor.com, or visit shelleybtxrealtor.com to get started. Who you hire matters — and I’d love to earn your trust. |

Shelley Broussard, REALTOR® | ABR® | SRS® | SRES® | RENE | TRLP

Real Broker, LLC | Serving Pearland, Friendswood, League City & Greater Southeast Houston

832-890-3504 | shelley@shelleybtxrealtor.com | shelleybtxrealtor.com

Categories

- All Blogs (90)

- Builder (2)

- Buyer (29)

- Closing Costs (7)

- First Time Home Buyer (13)

- Friendswood Neighborhoods (19)

- Houston Neighborhoods (18)

- Incentives (7)

- Just Fun (2)

- League City Neighborhoods (19)

- Manvel Neighborhoods (19)

- New Construction (3)

- New Homes (5)

- Pearland Neighborhoods (14)

- Real Estate (30)

- Real Estate Agent (15)

- Realtor (10)

- Relocation (16)

- Seller (28)

Recent Posts